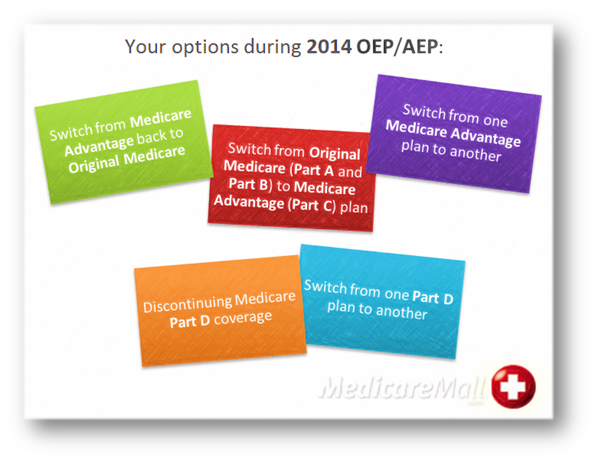

We’ve often described the Oct. 15-Dec. 7 Medicare Open Enrollment Period (OEP), a.k.a. Annual Election Period (AEP), as a great opportunity to evaluate your current Medicare coverage and consider certain changes in coverage for the new year.

Without a doubt, it’s important during the OEP/AEP to know what coverage you need for the new year, but it’s just as important to be a shrewd shopper who gets the best coverage at the best price.

Here are seven tips to help you be a smart shopper during Medicare Open Enrollment.

- Look at what you’ve been paying for your current coverage. To get a true dollar amount, include premiums, deductibles, copays, and coinsurance charges. It’s important to keep careful records so that you can figure out exactly what your current coverage is costing you. Once you’ve got all the figures, add them up—and if the total exceeds your budget, it’s probably time to make a change.

- Look at upcoming changes to your current plan or plans. Remember that changes in Medicare plan details can occur from one year to the next. If your plan has informed you of any changes for next year, evaluate those changes carefully. By how much will your costs increase? Will your coverage or network options change? If there’s any change you don’t understand, contact your plan and make sure every detail is clear. Knowing how well your plan has served you in the past is important, but it’s more important to know how well your plan is likely to serve you in the future.

- Look at changes in your circumstances. Have you won the lottery—or are you looking for new ways to stretch a dollar? As budgetary considerations change, it’s a good idea to fine-tune your Medicare coverage. Changes in your health circumstances have to be taken into account, too. Will you need coverage in a new area of your health next year? Are you taking any new prescription drugs? Lay out every significant change that has occurred in your life since you chose your current coverage, and then determine whether a change in coverage seems to be in order.

- Determine how well your current coverage is likely to serve you next year. Taking into account everything we’ve discussed so far, try to figure out where your current coverage would leave you a year from now. Why a year from now? That’s because Medicare Open Enrollment takes place only once a year, and this year’s Annual Election Period may be your only chance until this time next year to make certain changes you ought to make in your Medicare coverage. Putting off a change likely to save you money over the course of a year can cost you thousands, so it’s important to try to get a picture of where your current coverage would likely leave you a year from now.

- Compare other plans to your current plan or plans. This is where being a shrewd shopper really kicks in. Once you know how well your current coverage has served you, and is likely to serve you in the future given your current circumstances, needs, and expectations, it’s time to consider whether a new plan or plans may be more suitable. Check out the various Medicare Advantage, Medicare supplement, and prescription drug plans to determine which plans available in your area appear to offer the best fit for next year. Perhaps you’ll find a Medicare Advantage plan that offers coverage in an area of health that has become a concern for you. Perhaps you’ll be drawn to Medigap Plan F and its ability to eliminate most or all out-of-pocket costs. Or perhaps, after comparison shopping, you’ll decide that your current coverage is still your best option for next year.

- Compare the cost of plans available in your area. Getting the right coverage for next year isn’t just a matter of choosing the plan best suited to your current circumstances. Prices for the very same plan can vary widely from company to company, so failing to compare rates offered by the leading companies in your area can cost you dearly. It can also be costly to assume that, since a company offers the best rate for one plan, it is going to offer the best rates across the board. Look up the rates for individual plans, and avoid costly assumptions.

- Discuss your Open Enrollment options with a licensed professional. There is no obligation and no cost, but the savings may be substantial. An experienced professional may be your best resource for maximizing coverage and savings in 2014. Annual Election takes place only from Oct. 15-Dec. 7 of each year, remember, so failing to take full advantage of this year’s Open Enrollment by consulting a professional Medicare plans representative could cost you thousands of dollars over the next year.

Do you have another shopping tip for Open Enrollment? Please leave a comment!

© 2013 MedicareMall.com